It seems like everybody’s talking about governance these days: data governance, the principles that are addressed in the DAMA-DMBOK [1]; BI governance, including many of the issues covered in my book Growing Business Intelligence [2]; and now AI governance, an emerging topic of increasing concern to data and BI professionals. What do they do? How are they similar? How are they different? And how do we actually implement them?

I’d like to begin addressing these topics by asking and answering a simple question: What is “governance”? Of course, there are many formal definitions of this word, including Robert Seiner’s [3]. But let me suggest a simpler, if less formal, definition: Governance means ensuring that any given asset is quickly and easily available in a usable form to authorized individuals to be used in creating business value.

This definition syncs pretty well with Seiner’s own definition of data governance: “The formal execution and enforcement of authority over the management of data and data-related assets.” It is also reminiscent of a credo that was very popular with data professionals 30 or 40 years ago: “The right data at the right time, in the right form, to the right people.”

But Seiner’s definition highlights a very important truth: Governance is asset management. And once this truth is understood, a lot of the mystery around governance clears up, and the necessary approaches to governance become much easier to understand.

Data Governance Deep Dive

Learn how to design, implement, and evolve data governance programs while preparing for the CDMP specialist exam – Aug. 3-5, 2026.

I discussed many of the fundamental truths of asset management (especially the management of data assets) in a series of TDAN articles [4] published in December 2023 and January 2024. In one of the articles, I make the following point about assets:

An asset can be defined as a resource that can be managed in such a way as to create some sort of value (or benefit) for an enterprise. The generated value, in turn, can be managed in ways that give an organization some kind of competitive advantage. Both the asset and the generated value of the asset must be manageable, and the economic benefit of the asset must be measurable. [5]

So, governance involves the conversion of resources into business assets. One question I’m often asked is whether data is an asset or a resource. In my view, data is a resource that becomes an asset when it’s managed in a way that creates business value. But the process that converts data from a resource to an asset is an asset management process, the exact same process that manages the asset once it’s created. So, the real business asset is not the data per se, but rather the data management process that converts data resources into business assets. This is why I don’t have a problem with people who talk about “managing data as an asset.”

And I think this is true of all asset management. The business value is created not from the assets (or resources) themselves, but rather from the way they are managed. I’ve made the point that resources themselves are not business assets, even if they are entered as such in an accounting ledger. A building may be entered in the ledger as an asset, but if the building is just sitting there not being used, it’s an expense, not an asset. You’re paying property taxes and maintenance and upkeep, and it’s not bringing in any revenue. You can own a fleet of trucks, but if you’re not using them, you’re just paying for maintenance and depreciation. Only when resources are managed in a way that creates business value do they actually become assets. And this is true of data as well. Data just sitting in a database or file is a cost to the business, unless that data is being used to create business value.

In other words, nothing is an asset per se; something only becomes an asset when it is managed in a way that creates business value.

Another important point is that asset management often involves the transformation of the asset in some way. The management of data, for example, involves transforming data into streams of information, which are then subsequently transformed into knowledge assets. So, an important question to ask is: What transformation(s) of a resource are necessary to turn it into a business asset? It is often said that data is the “new oil” or the “new water,” and if that’s true, it’s true in part because some sort of processing or refinement is necessary to convert raw data into a usable and consumable form.

A third point is that assets contribute business value by either creating, supporting, or disrupting business processes. Assets become, in the parlance of business process reengineering, either “essential enablers” or “essential disrupters” of business processes [6]. As people like David R. Vincent [7], Jeffrey Rayport, and John J. Sviokla [8] have noted, business value is created when information-based business processes are used to reimagine the ways in which a business interacts with its customers, suppliers, regulators, and other critical stakeholders. Business value is further created when these processes empower stakeholders to do things for themselves, rather than have to wait for others to do things for them.

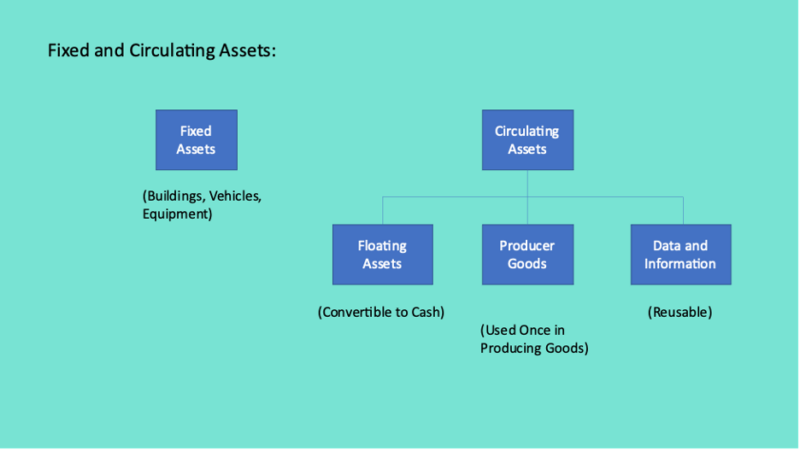

I’ve made the point before that data is a special type of asset, a circulating asset as opposed to a fixed asset (see illustration below). As such, data assets have special characteristics that require them to be managed in a specific way:

- Data is not consumed as it is used, can exist in multiple places at the same time, and can be combined with other data to create entirely new data assets. As such, data needs to be managed for reusability. The business value of data is directly proportional to the degree to which it can be shared and reused to support multiple business processes and multiple business initiatives.

- Data only has value when some sort of context (i.e., metadata) is provided that enables the business to understand its meaning and gauge its usefulness and application to a given business need. Context is what enables Data to be “refined” into a useful form; without context, Data is just so much useless sludge.

- There is a fitness for purpose requirement for data that doesn’t exist for other types of assets. We never, for example, need to ask whether a $20 bill is “fit” for buying something. But we very much have to know whether a given set of data is “fit” for some intended business purpose.

- Because the business value of data is directly tied to its sharing and reuse, it follows that the management of data must be concerned with data in motion, rather than data at rest. Data just sitting in a data repository does not create business value. Business value is only created when the data is in motion, being used to create streams of information content that link together business stakeholders and create knowledge assets.

Finally, it’s important to understand that asset management is not so much about the management of assets per se as it is about the management of people’s behavior with respect to assets. We don’t manage money so much as we manage the behavior of people with regard to spending, and the reporting of their spending. An inventory manager controls when new inventory is ordered, and in what quantities, and where and when it’s delivered. What data managers manage are the processes by which data assets are acquired, evaluated, enhanced, provisioned, used and (eventually) disposed of, in ways that ensure the maximum amount of value at least cost for the company. Asset management is never the management of things – it is always the management of people and processes [9].

These principles of asset management provide the basis for understanding how data governance (and also BI and AI governance) should be approached. I’ll drill down deeper into these governance issues in the next article. Stay tuned!

[1] See my TDAN article, “Thoughts on the DAMA DMBOK.” June 18, 2025. dataversity.net/articles/thoughts-on-the-dama-dmbok/

[2] Burns, Larry. Growing Business Intelligence (Technics Publications LLC, 2016).

[3] Seiner, Robert. Non-Invasive Data Governance (Technics Publications LLC, 2014), pp. 2-4.

[4] Burns, Larry. “The Currency of Information” series of articles for TDAN. The fourth article in the series can be found at: dataversity.net/articles/the-currency-of-information-measuring-the-value-of-data-part-four/. Hyperlinks to the other three articles can be found in the opening paragraphs.

[5] Ibid, Part 1.

[6] Hammer, Michael and James Champy. Reengineering the Corporation: A Manifesto for Business Revolution (HarperCollins Publications, 1993), pp. 40-44.

7] Vincent, David R. The Information-Based Corporation: Stakeholder Economics and the Technology Investment (Dow Jones-Irwin, 1990).

[8] Rayport, Jeffrey F. and John J. Sviokla: Exploiting the Virtual Value Chain. Harvard Business Review, November-December 1995, pp. 75-85.

[9] “The Currency of Information,” Part 2, op. cit.

Applied Data Governance Practitioner Certification

Validate your expertise and take your career to the next level.